Sonic’s Early Vertical Integration Revenue Outpaced Fee Burns By 400%

On March 1, 2026, Sonic began an early run of its Vertical Integration (VI) thesis.

Vertical Integration marked a shift in how Sonic thinks about L1 value capture: transaction fees alone are not enough for a modern network. As execution gets cheaper by design, gas fees become a weaker economic base. That is better for users and applications, but it also means networks need another way for activity to accrue value back to the native asset.

Sonic is approaching this through product-level revenue from native financial infrastructure. Instead of leaving the network dependent only on gas, owned and aligned products can contribute directly to S-aligned value capture.

The Early Comparison

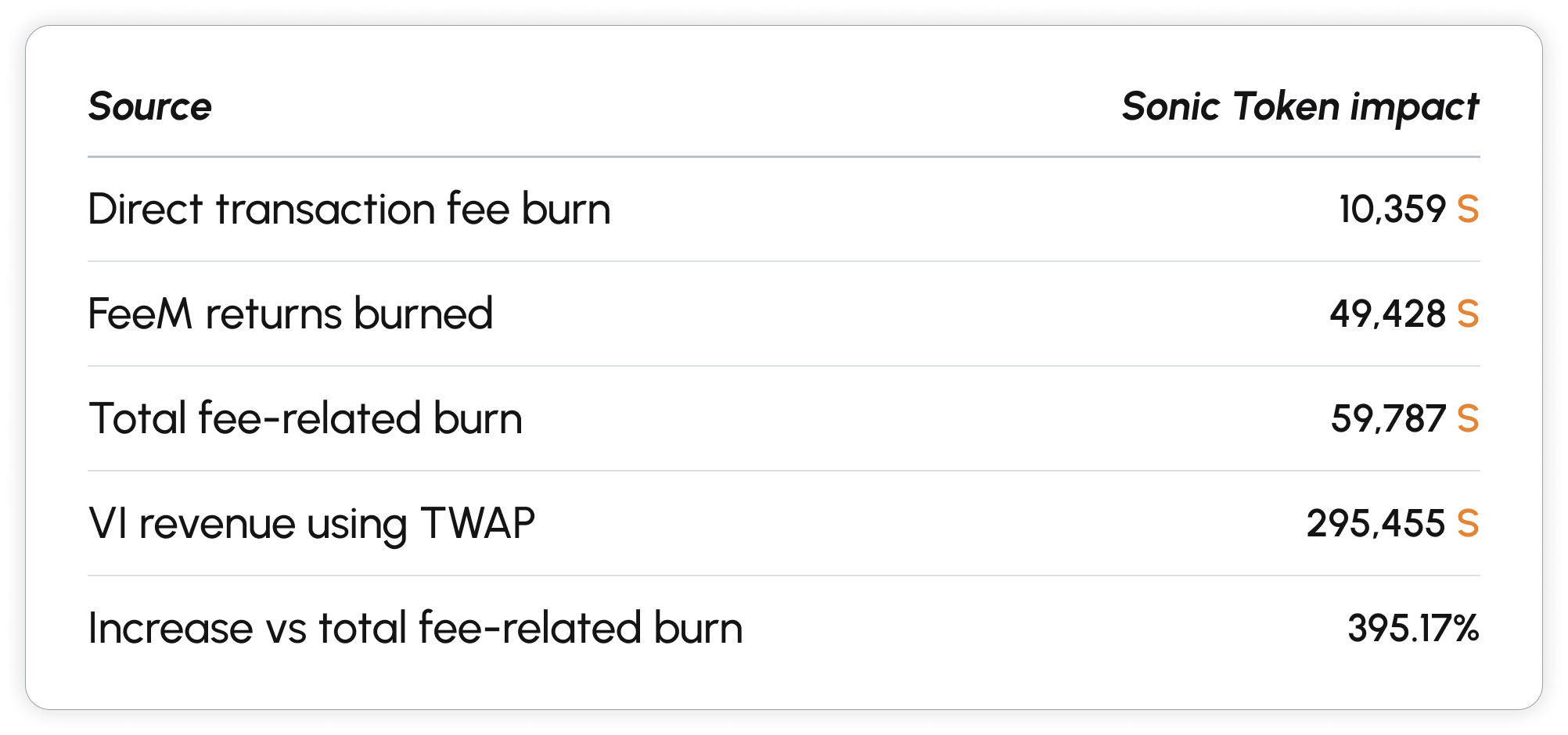

The first numbers are not large, but they are useful. Since March 1, Sonic’s minimal VI implementation has generated $13,000. Using the TWAP price since March 1 of $0.044, that equals 295,454.55 S.

Over the same period, total fee-related burns were 59,786.728 S. This includes 10,358.726 S from the direct transaction fee burn and an additional 49,428.002 S from FeeM returns burned.

That puts the early VI base at roughly ~400% the deflationary impact of total fee-related burns.

A Narrow First Implementation

This is still a narrow implementation of Vertical Integration. The current revenue comes from USSD and Metropolis vault activity, while the broader model has not started scaling yet and most network-aligned revenue lines are still ahead.

This is still early, but it is enough to show the direction. If this is possible with a narrow implementation, the model becomes more interesting as more product surfaces begin contributing revenue.

The Limit of Fee-Based Value Capture

Sonic still burns a portion of transaction fees. But on a high-throughput chain, gas should remain cheap. The network should not need expensive execution to create value for the native asset.

A chain that only sells blockspace is tied to transaction pricing. If fees are high, users and applications feel it. If fees are low, the fee-burn model becomes smaller.

Product revenue gives the network another path. Users can still get cheap execution, while revenue from Sonic-aligned financial products contributes back to the network economy.

Reading the Signal

The point is not that $13,000 is a major revenue base. It is that a small, early version of VI has already produced a much larger deflationary impact than fee-related burns over the same window.

This makes it a successful early proof of concept for Sonic’s Vertical Integration model. The mechanism is live, and the first result is already measurable.

As blockspace gets cheaper, L1 value capture has to rely on more than gas. Fee burns remain useful, but the larger opportunity is product revenue tied directly to network activity.

The full VI model has barely started. This first data point shows the direction.

Methodology: VI revenue is converted to S using a $0.044 TWAP for the analysis window from March 1 to May 11, 2026. Transaction fee data covers epochs 66,898–77,162 and blocks 63,976,841–70,192,289.

Total transaction fees rounded from WEI were 207,174.525 S. The split is 90% FeeM Treasury, 5% validators, and 5% burn, with 10,358.726 S burned directly. In the same block range, FeeM returned 98,856.004 S, split equally between rewards and burns, adding 49,428.002 S burned. Total fee-related burn used for comparison: 59,786.728 S.

VI impact: $13,000 / $0.044 = 295,454.55 S, roughly 4.94x the total fee-related burn amount.